When New York City comptroller Scott Stringer announced his mayoral campaign on September 8, he pledged that under his administration, there would be “no more giving away the store to developers.”

“No more unaffordable affordable housing,” he said. “We will put an end to the gentrification industrial complex and end policies that perpetuate a cycle of segregation in our neighborhoods.”

But public pension fund investments made under Stringer’s watch heavily subsidized private equity real estate—and cost the city hundreds of millions of dollars when they underperformed.

As comptroller, Stringer oversees the investment strategy of the New York City Employees’ Retirement System (NYCERS), the city’s largest pension fund. During Stringer’s tenure, NYCERS has scaled up its investments in high-fee, high-risk private equity real estate.

From 2016 to 2019, NYCERS increased its portfolio in private equity real estate by 45%. This included the investment of $150 million of new assets into the Blackstone Group, a private equity firm which has been accused by the UN of contributing to the global housing crisis through its aggressive eviction practices and dramatic rent hikes.

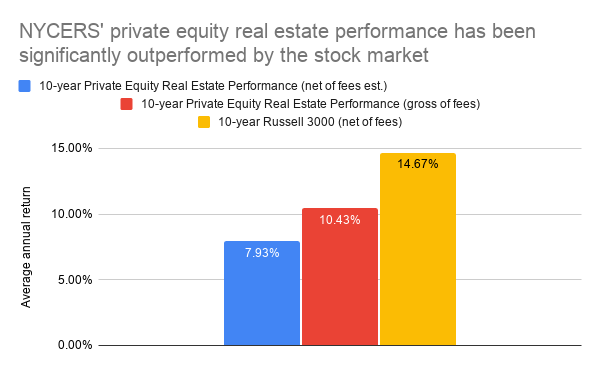

Returns on these investments have significantly lagged the stock market. A New York Focus analysis of NYCERS’ annual reports from 2016 to 2019 has found that investments in private equity real estate have cost the city over $260 million in lost performance relative to the stock market, in addition to $110 million in reported fees, for a total of at least $370 million.

“Even on the reported values, NYCERS’ private equity real estate portfolio has dramatically underperformed,” said Edward Siedle, a former Securities and Exchange Commission attorney who received the largest whistleblower award in the agency's history in 2019.

When the pension underperforms, the cost is ultimately borne by city taxpayers, whose annual contribution to the pension fund is determined based on returns. Smaller returns means that a larger part of the city budget is allocated to pensions.

This means that money that could have been used to repair public housing or ensure ventilation in the city’s schools is now making up a shortfall generated by poor performance by Wall Street money managers.

High fees and poor performance

Jeff Hooke, an investment banker and senior lecturer at Johns Hopkins University, said that the $110 million in reported fees is a significant underestimate of how much the city actually pays in fees.

Accounting for fees like the carried interest fee, which NYCERS does not report, Hooke’s research has found that “fees are 2.50% of private equity assets under management, not 1% or 1.5% as indicated” in the pension fund’s annual reports. The actual amount the city paid in fees to private equity real estate firms from 2019 to 2019, in other words, may be as high as $183 million.

Officially, NYCERS’ 2019 financial reports show a 10.43% annualized return for its private equity real estate portfolio over the last decade, clocking in at 71% of the Russell 3000 stock index’s annualized return of 14.67%. But because the pension fund reports its 10-year returns without accounting for fees, the actual performance of the portfolio is even lower. Applying Hooke’s estimate of 2.5% fees, NYCERS' private equity real estate investments have earned the city just 55% of what it would have made investing in the Russell 3000.

Even this lower estimate could be overestimating NYCERS’ performance, because it relies on asset values calculated by the money managers themselves. Private equity real estate, Siedle said, is “highly susceptible to inflated valuation because the values are unilaterally determined by the managers.” Based on decades of experience in pensions, Siedle typically presumes that reported performance is likely worse than reported—and never better.

“Real estate is one of the least transparent investments,” Siedle concluded. “it has all kinds of hidden and embedded fees, and remarkably there’s been less scrutiny of real estate fees than even standard private equity fees.”

“Just give money to a gambler and send them to Vegas”

Why do pension funds continue to invest in an industry that performs so poorly? Finding information about the pension fund’s decision-making process can be difficult; unlike nearly every other major public pension fund, NYCERS does not post its minutes online.

Stringer’s office did not respond to a detailed list of questions sent by New York Focus. In 2015, as this writer reported at the time, Stringer strongly pushed for a change in state law that would have allowed a larger expansion into private equity real estate and other so-called “alternative investments.” Investing more in these areas, said Stringer's spokesman, “will allow the pension boards to achieve a superior risk-adjusted return.”

Many pension funds justify investments like private equity real estate by arguing that they are not correlated with broader stock and bond markets, and thus add diversity and protect against risk. As the alternative investment data company Preqin wrote in a 2016 newsletter, “real estate remains a crucial part of many pension fund portfolios, with investments in the asset class able to mitigate against fluctuations in traditional bond and stock markets.”

But according to Siedle, this argument holds little water.

“If you want an investment that does not correlate with traditional stocks and bonds, just give money to a gambler and send them to Vegas,” he said. “Those won't correlate and thus mitigate the fluctuations of the market. It all depends if you’re willing to take on that risk.”

“Publicly traded investments have clearly ascertainable values and clearly ascertainable performance,” Siedle added. “The minute you migrate away from the public market, you're incurring substantially greater risk. As a prudent fiduciary, the question is: Can you justify that divergence or that migration? You should expect returns that substantially outperform public markets given the risk.”

Managing the pension funds is arguably the comptroller’s most powerful role, but Stringer’s record on pensions has thus far avoided media scrutiny. The comptroller sits on the boards of all five city pension funds, which currently have $221 billion in assets, and employs and supervises the investment staff of the pension funds in the Bureau of Asset Management. NYCERS’ board also has representation from the city’s mayor, public advocate and borough presidents, and the major city labor unions, which must approve investments.

City Council Member Brad Lander, who is running for comptroller, said he would look at the performance of private real estate and other alternative investments if elected. “The pension funds need to be invested in a way that maximizes long term value and minimizes fees,” said Lander. “We need to take a good hard look at whether private equity firms do that.”

Pension fund investments in private equity have long been tainted by corruption. The city’s first major commitments into alternative investments were led in the 1990s by then-city comptroller Alan Hevesi, who later went to prison for receiving bribes to place alternative investments with the state pension fund as state comptroller. Hevesi also accepted large campaign contributions from Blackstone’s CEO, Stephen Schwarzman, even as the firm won lucrative contracts from the state pension fund. The SEC banned these types of contributions in 2010.

Beyond Blackstone, private equity real estate investments made on Stringer’s watch include $90 million to the Carlyle Group, whose executives were found to have bribed Hevesi, and $260 million to Brookfield, a secretive real estate firm that owns large swaths of the city’s real estate and recently courted congressional investigation by bailing out the family of Jared Kushner from its debt-laden investment on 666 Fifth Avenue.

“You can’t run for mayor on real estate speculation”

Beyond the concerns about underperformance, high fees, and opacity is the social impact of the investments. Cea Weaver, coordinator of the Housing Justice for All coalition, which played a leading role in securing the landmark 2019 expansion of renter’s rights, pointed out that housing activists are almost always battling with Brookfield and Blackstone. The city’s investments in these firms, she argued, give rise to a major conflict of interest on housing policy.

“Brookfield is really invested in rent stabilized housing, and there is this problem where in order for these portfolios to do well, they have to evict rent stabilized tenants,” said Weaver.

Weaver pointed out that the change in rent regulations upended the future values of many private equity real estate managers’ properties, because it barred them from turning some rent stabilized apartments into market rate housing.

“The rent laws changed the speculative value of one million apartments in the city with ramifications for private equity investors,” Weaver said, pointing to Brookfield’s investment in a portfolio of rent-stabilized apartments in East Harlem as one example.

“Blackstone owns Stuy Town, where they have effectively stopped doing repairs. From my perspective, there’s this massive problem,” Weaver added. “If we succeed politically the investments will do worse. The reason why Stringer should be divesting from real estate is because tenants’ political agenda is at odds with them.”

“You can’t run for mayor on real estate speculation,” Weaver concluded. “He needs to not be a participant in it.”